Before the COVID-19 pandemic gripped the world in early 2020, office social events were a core component of the on-premises working experience. From potluck lunches to happy hours, office holiday parties to corporate outings to sporting events to concerts, anyone working in a traditional office setting knew that their calendar would often include “optional” office events outside the 9-to-5 workday. Depending on the workspace, these events could be something that everyone looked forward to, or something everyone rolled their eyes at when they saw the next email invitation in their inbox. Love them or hate them, the office social life was a standard part of the pre-pandemic corporate experience.

Fast forward three years later, and the entire traditional corporate work environment looks nothing like it used to. Evidenced by vacant downtowns and high-rise buildings in major cities, as well as fully remote or hybrid organizations with thousand of employees, few could have envisioned that the coronavirus would have some fundamentally transformed traditional office culture in so many ways. And office event planning is no different.

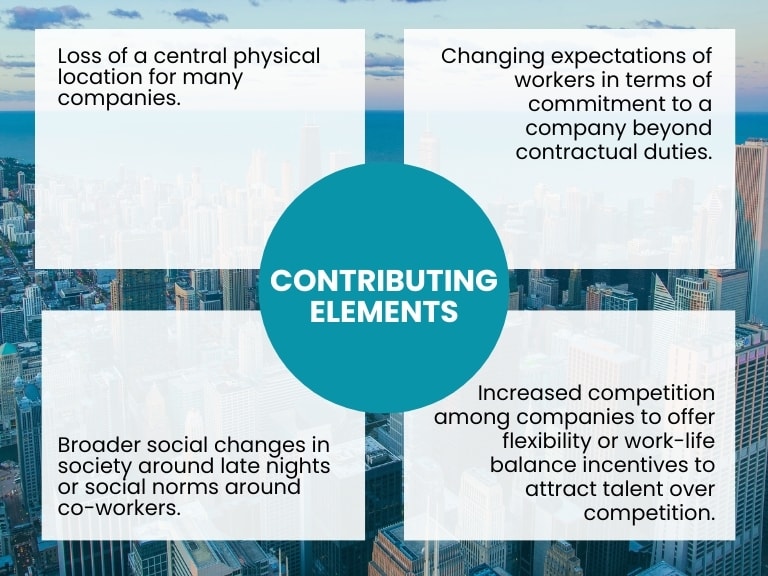

There’s no single factor that explains the new landscape of office social culture, but here are some of the contributing elements:

Regardless of the central driving factor, the economic impacts of this shifting office social culture are real and visible. Cities like San Francisco and Chicago frequently make headlines for their struggling downtowns and related hospitality sectors. City officials and planners are introducing a variety of programs to attempt to reshape their economic foundations as a result. So far, the results are at best a mixed bag.

In Part 1 of our series exploring how fundamental changes in office social culture and events continue to reverberate through society, we’ll look at the the economic scale of impacts being felt on a daily basis in the boardrooms and dining rooms of America’s downtowns.

Consider some of these statistics that reflect just how intertwined office social culture and downtown economies were pre-COVID, and the measurable impacts on different economic sectors since office events and social lives underwent their COVID-induced upheaval:

As if the current data wasn’t telling a troubling story already, the numbers that are truly concerning economists and business leaders are those with an eye on the future. Beyond the empty storefronts and empty offices, the ripple effects of changing office culture also have the potential to cause economic damage that could spread far beyond downtown business districts.

Skyrocketing interest rates thanks to frequent Fed rate hikes have made previously cheap debt a ticking time bomb for all borrowers, but particularly for commercial real estate companies. Vividly illustrated by the recent bankruptcy of WeWork, companies who had been taking advantage of cheap money to finance downtown real estate purchases now face a double whammy of empty offices (and thus, declining rents) and rising debt costs on their balance sheets.

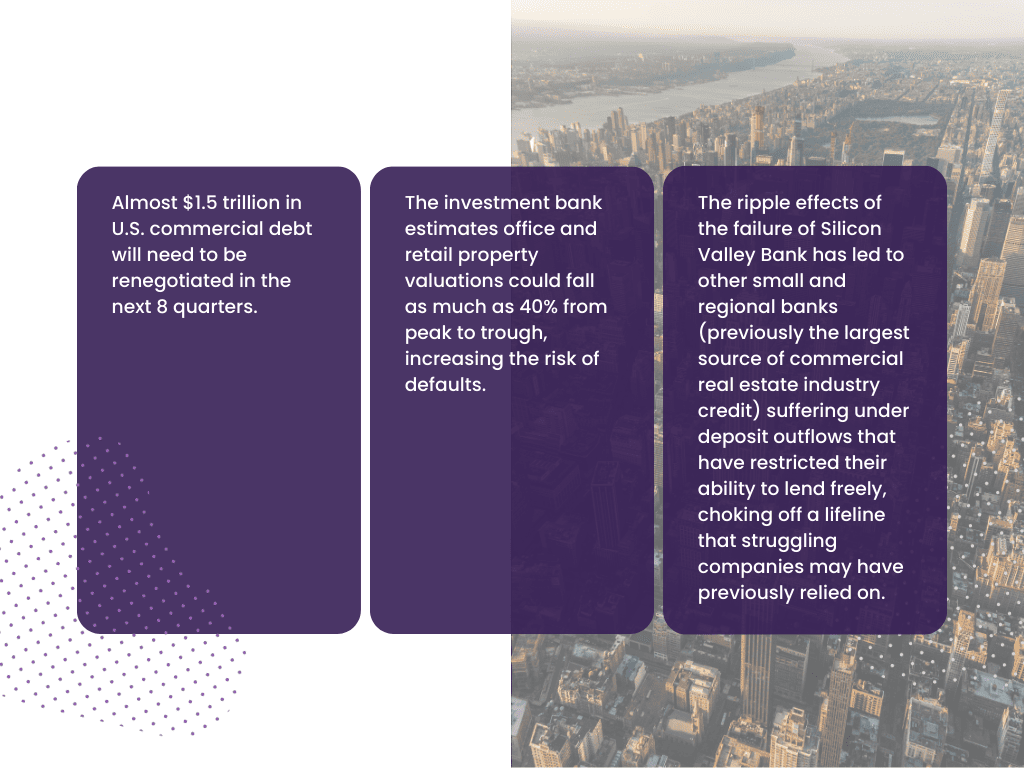

This has led to many economists pointing to commercial real estate as a ticking time bomb. Considering the pure size of the commercial real estate industry as part of the global economy, a series of bank and management company failures could have a catastrophic impact on other intertwined elements like pension funds and civic budgets. It’s hard not to think of the 2008 sub-prime mortgage crisis as a potential model for what this may look like. Consider some of the numbers from a report published by Morgan Stanley in April:

Beyond the commercial real estate market is a similarly brewing crisis in the hospitality industry that, coupled with the loss of office social culture and revenue from after work dinners and drinks, creates an equally worrisome long-term forecast. Data around the hospitality and events industries worldwide since the pandemic reveal an array of challenges for business owners:

The challenges facing city officials, CEOs, hospitality professionals, and commercial real estate managers are different in size and scope. But the unifying factor of a fundamental shift in office culture and social life remains the same. While the data paints a troubling picture, there remain unanswered questions. The answers to these questions may be the difference between a slow recovery to a “new normal”, or a future where the most problematic trends become reality:

Share

Get the latest product updates, event planning tips, and industry insights — straight to your inbox.

You can unsubscribe at any time. Your email will only be used to send RSVPify updates and will never be shared.